Know which partner does what before you commit budgets.

ℹ️ Glossary: Acronyms in this article

• KPI — Key performance indicator.

• OI — Off-invoice discount taken by the buyer.

• MDF — Market development funds for retailer-facing promos.

• TPR — Temporary price reduction at shelf.

• POS — Point-of-sale scanner sales data.

• OOS — Out-of-stock; no inventory on shelf/DC.

• MOQ — Minimum order quantity.

• SLA — Service level agreement (response/performance).

• DC — Distribution center.

• GTN — Gross-to-net: revenue after discounts/trade.

• PPA — Price-pack architecture (sizes/prices for retail).

• Banner — The retail chain brand (e.g., Kroger, H-E-B).

• Void — Store is authorized but item isn’t selling(missing/uncoded).

You only scale once; at least you only want to pay for it once. The wrong partner combo drains trade dollars, slows sell-through, and adds chaos to your forecasts. Use this fast framework to vet brokers, distributors, and sales rep organizations so your first big push has the best chance to stick.

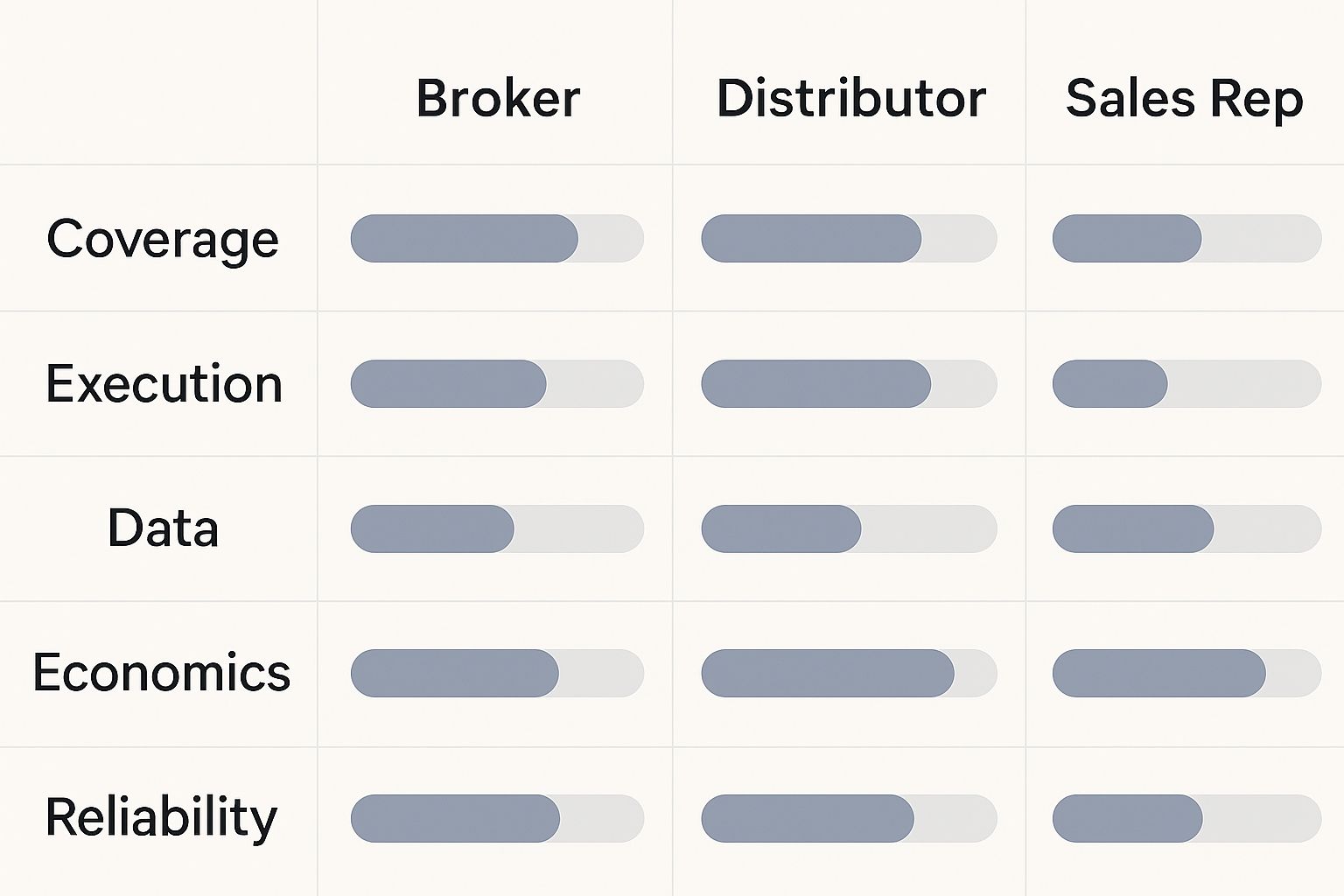

• Coverage reality: Which retailers, geographies, and categories they actively move, not just “have relationships” with.

• Proof of pull: Recent authorizations, resets, or Temporary Price Reduction (TPR) wins they led in your price tier.

• Retail math alignment: How margins, fees, minimum order quantities (MOQs), and lead times affect your gross-to-net (GTN) and cash conversion.

• Execution muscle: Merchandising, audits, deductions management, data cadence, and speed to escalate issues.

• Conflict risk: Competitive lines, brand priorities, and territory overlaps.

• Pilot terms: Limited-scope test, clear key performance indicators (KPIs), and a clean exit clause.

Use a 1–5 score for each criterion and total it. Anything under 24 needs a rethink or a tighter pilot.

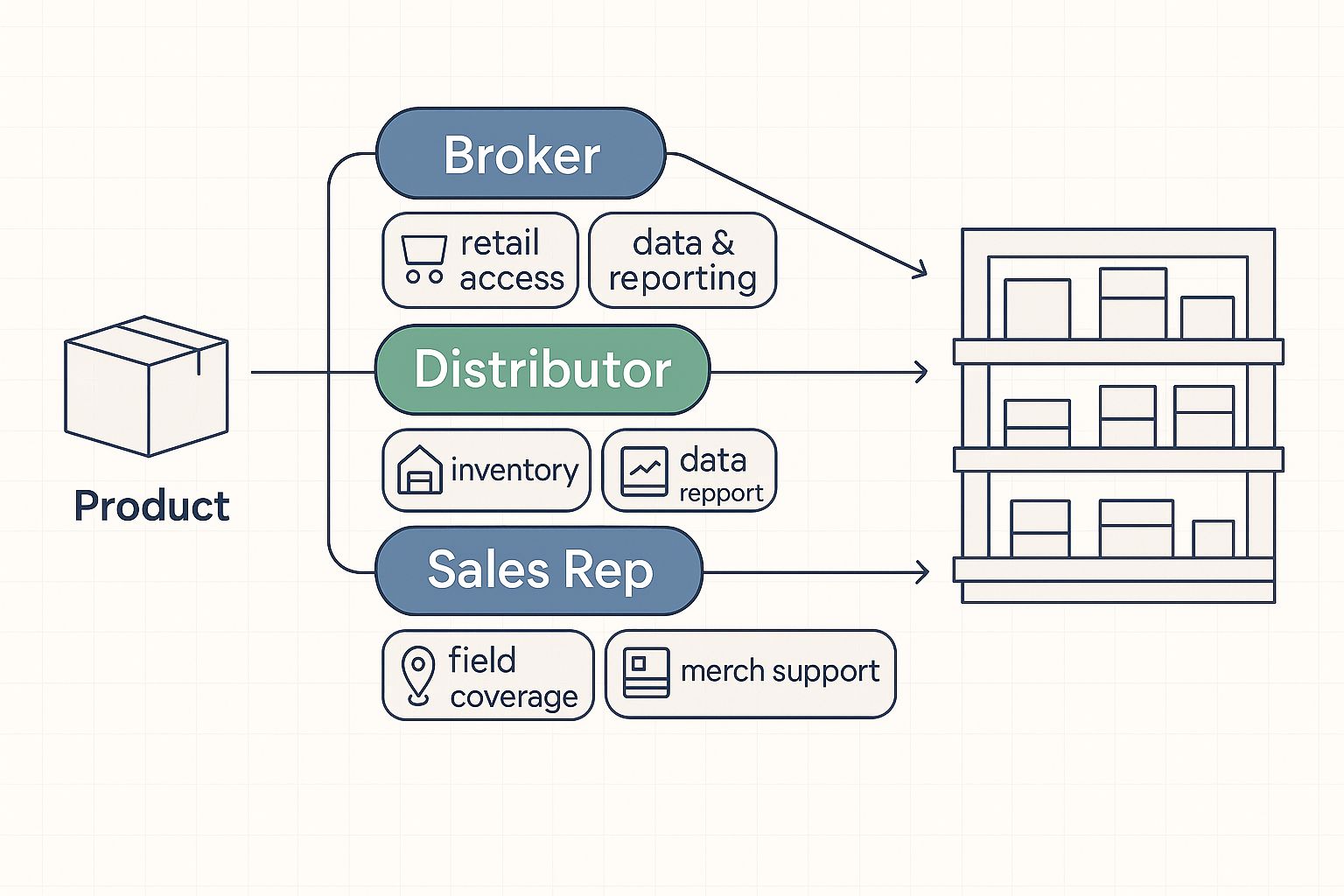

Broker: Commissioned intermediary focused on selling and managing the retail relationship. No inventory. You still own demand planning, logistics, and deductions handling. Good when you need access across many banners and can handle ops in-house.

Distributor: Buys and resells your product, holds inventory, and services stores. Expect added margin and MOQs, yet better reach into independents and small chains. Good when you need physical coverage fast and your case-pack economics can carry the extra layer.

Sales rep organization: Contract field sellers, often region-specialized, compensated by commission or retainer plus commission. Lighter footprint than a broker, but execution varies; you must clarify merchandising and data requirements.

Cost reality: Model your GTN with each path, including commissions or distributor margin, expected trade spend, freight, fuel surcharges, and expected deductions. If your unit economics crack under a realistic off-invoice discount (OI) plus market development funds (MDF) scenario, fix price or pack first, not after launch.

• Vague “relationships”: Ask for named buyers and the last three wins by category and banner.

• No store-level visibility: If they cannot show basic OOS and void reports, your resets will stall.

• One-size contract: You want pilot terms, service level agreements (SLAs), and data deliverables spelled out.

• Competitive overload: Too many similar brands equal diluted focus.

• Slow escalation: Ask them to walk you through a recent deduction dispute or distribution center (DC) short, who did what, and how long it took.

1) Define scope: 2–3 priority banners or 10–20 target stores, 90–120 days.

2) Set KPIs: On-time authorizations, weeks to first PO, shelf placement achieved, percentage of voids closed, OOS rate, promo compliance, and POS lift versus baseline.

3) Lock the data: Weekly cadence for POS, store lists, OOS, deductions, and photos.

4) Fund wisely: Align TPR, OI, and demos with your price architecture. Track GTN weekly, not quarterly.

5) Exit or expand: If they hit the marks, expand the scope. If not, exit cleanly and move on.

• Hidden distribution costs checklist to sanity-check your scale math. (Retail Distribution Hidden Costs [+ Planning Checklist])

• What retail buyers expect before authorizing your brand and plan. (Want to Land in Stores? Here’s What Buyers Expect)

If you want a second set of eyes on your partner options, we can help you quantify the risk, structure the pilot, and negotiate terms that protect your margin and momentum. Contact us below to get a practical plan you can act on this quarter.

[1] McKinsey & Company (2021). “How precision revenue growth management transforms CPG promotions.”

[2] GS1 (2023). “2D Barcodes at Retail Point-of-Sale Implementation Guideline.”

[3] GS1 US (n.d.). “Barcodes Available in GS1 US Data Hub (ITF-14 not for POS).”

[4] Specialty Food Association (2023). “The Basics Preview: Maximizing Broker, Distributor Relationships.”

[5] Montana Department of Agriculture (2024). “The Role of Distributors and Brokers.”

[6] Nielsen IQ via Food Manufacturing (2022). “Retailers Lost 7.4% in Sales to Stock-Outs in 2021.”

[7] National Agricultural Law Center (n.d.). “Perishable Agricultural Commodities Act (PACA) Overview.”