Where growth breaks when economics are misunderstood

Most emerging CPG brands miscalculate distributor economics by focusing on gross margins instead of true net revenue after distribution,retail margins, and trade spend. This leads to scaling models that appear profitable but lose money in practice. The key is understanding how margin compresses across the full system before expanding distribution.

Most emerging brands build their financial model around a number that does not actually determine success.

They focus on gross margin. See how pricing assumptions impact margin structure.

On paper, it makes sense. If a product costs $4 to produce and sells for $10 wholesale, the margin looks strong. That gap feels like room to grow, invest, and scale.

But that number exists in isolation. It does not reflect how money actually moves once a product enters distribution.

The moment a distributor is involved, that margin begins to compress. Then the retailer takes their share. Then trade spend begins to pull from what remains. Promotions, discounts, and deductions are layered in as a normal part of doing business, not as exceptions.

What looked like a healthy margin becomes something far thinner.

The mistake is not in the math itself. It is in what the math excludes.

Brands that model only gross margin are effectively making decisions based on an incomplete version of reality. And when those decisions translate into distribution, the gap becomes visible very quickly.

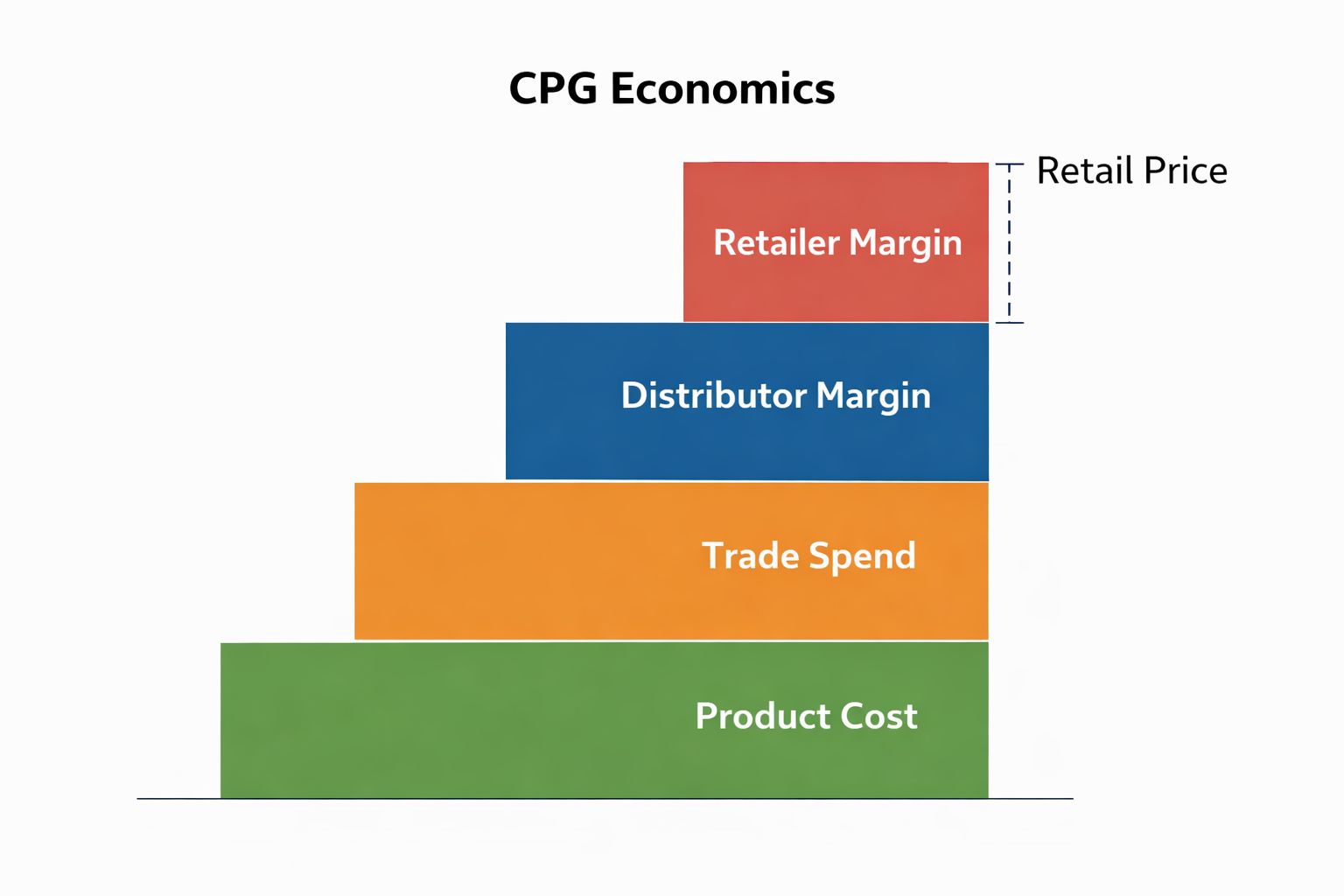

Understanding distributor economics requires a shift in perspective. It is not a single percentage to account for. It is a system of interdependent layers that shape what you ultimately earn.

Distributor margin is the first major shift. Typically in the 20–30% range, it is applied before most other downstream costs. This is not a negotiable expense in most cases. It is the foundation of how distributors operate.

From there, retailer expectations come into play. Retailers need their margin to justify shelf space, and that requirement directly influences your pricing structure. It limits how much flexibility you have before the product even reaches the shelf.

Then comes trade spend, which is where many emerging brands lose control of their economics. Promotions, temporary price reductions,bill backs, and marketing contributions are not occasional expenses. They are part of the operating model.

By the time all of these layers are applied, the original margin has been reshaped multiple times.

The critical point is that these elements do not operate independently. They stack. Each one reduces what remains from the previous layer, not from the original number.

Brands that understand this treat pricing, margins, and trade strategy as a unified system. Break down how trade spend fits into that system. Brands that do not tend to evaluate each component separately, which leads to overly optimistic assumptions.

Most founders experience distribution as a signal of success.

More accounts open. Revenue increases. The brand gains visibility. From the outside, it looks like the model is working exactly as intended.

But distribution does not fix economics. It scales them.

If margins are slightly weaker than expected, that weakness compounds with every new account. If trade spend is underestimated, it expands alongside distribution. If operational costs are not fully accounted for, they rise with complexity.

This is why some brands encounter a difficult paradox. Sales are growing, but cash becomes tighter. This is a common scaling issue in CPG distribution. The business appears stronger externally while becoming more fragile internally.

The underlying issue is not growth itself. It is that scale increases exposure to the full system of distributor economics.

Any flaw in the model becomes more pronounced as distribution expands.

Brands that move too quickly into new accounts without validating their economics are not just growing. They are accelerating the consequences of incomplete assumptions.

The most important transition an emerging brand can make is moving from gross margin thinking to net revenue thinking.

Net revenue reflects what remains after distributor margins,retail expectations, trade spend, and deductions are applied. Learn how pricing decisions affect net outcomes. It is the number that determines whether a business is actually viable at scale.

This requires a more disciplined approach to modeling.

It means treating distributor margin as a baseline assumption. It means incorporating trade spend as a standard operating cost rather than a variable decision. It means anticipating deductions and operational costs that come with growth.

More importantly, it shifts how decisions are made.

Instead of asking how to increase distribution, brands begin asking whether that distribution is economically sound.

They evaluate accounts, promotions, and pricing structures based on what they contribute to the business, not just the revenue they generate.

This shift creates clarity.

It reveals which parts of the business are truly working and which are quietly eroding margin.

Without this perspective, growth can mask underlying issues.With it, growth becomes intentional and sustainable.

Sustainable distribution is not defined by how quickly a brand expands. It is defined by whether that expansion strengthens the business.

That starts with clarity around fully loaded costs,realistic margin expectations, and the true impact of trade spend before entering new accounts. See how to structure expansion correctly.

From there, discipline becomes essential.

Not every opportunity should be pursued. Some accounts require pricing or promotional structures that do not support long-term profitability. Some expansions introduce complexity without improving financial outcomes.

Strong brands recognize these tradeoffs early.

They prioritize alignment between their economic model and their distribution strategy. They choose partners and channels that reinforce their margins. They make decisions that support the long-term health of the business, even when it slows short-term growth.

Over time, this creates a more resilient model.

Distribution becomes more predictable. Trade investments become more strategic. Growth becomes more controlled.

For founders and decision-makers, this is the difference between scaling a brand and building a sustainable business.

For strategy or implementation support, contact us below.

1. FMI – The Food Retailing Industry Speaks 2023

2. NielsenIQ – Trade Promotion Optimization in CPG

3. McKinsey & Company – Winning in US Grocery Retail

4. Circana(IRI) – The State of CPG Growth and Promotion